Offset vs Redraw: Which One Is Better for Your Home Loan Strategy?

Offset vs redraw is one of the most important decisions you’ll make when setting up your home loan. Interestingly though, most people don’t fully understand the difference until it’s too late.

The good news is, explaining offset vs redraw is not that complicated. On the surface, they can look similar, plus both can help you reduce interest and manage your loan more efficiently. However the way they work, and the impact they can have on your long-term strategy, is very different.

So let’s break it down simply.

What Is an Offset Account?

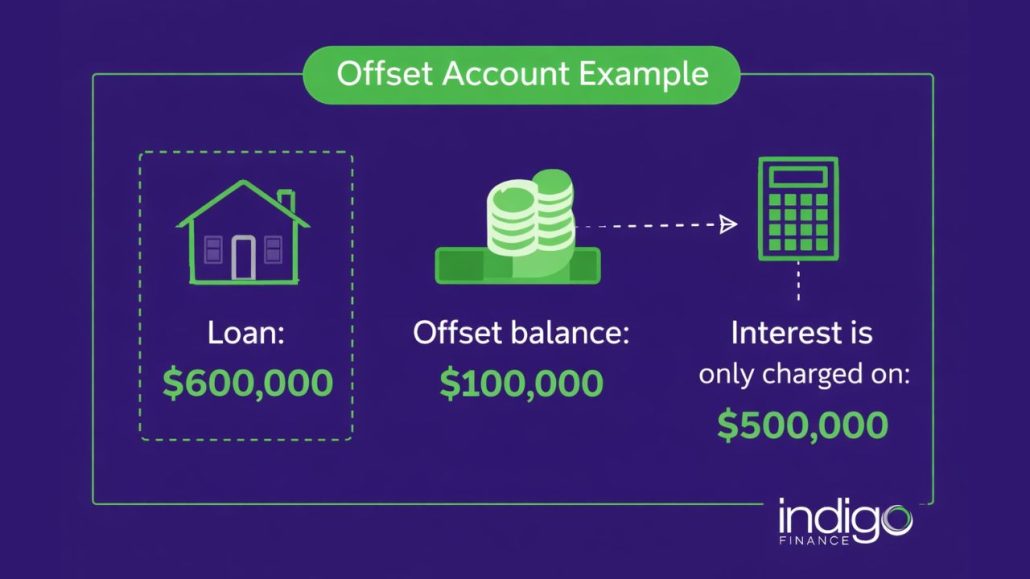

An offset account is a separate bank account that is linked to your home loan.

The balance in this account “offsets” your loan balance when interest is calculated.

In the example above, you still have full access to that $100,000 at any time, just like a normal savings account.

The key benefits of an offset account:

- Reduces the interest you pay without locking money away

- Full flexibility to access your cash anytime

- You can attach a credit or debit card to the account

- Can be powerful for long-term wealth building

- Clean structure for tax purposes (especially for investors)

What Is a Redraw Facility?

A redraw facility lets you access extra repayments you’ve made on your home loan.

Instead of sitting in a separate account, any money you pay into the loan above the agreed minimum monthly payment remains accessible to “redraw”.

Meaning, as an example:

- Loan: $600,000

- You’ve paid an extra $100,000

- Your loan balance becomes: $500,000

- Interest is only charged on: $500,000

- You may be able to “redraw” that $100,000 later

Sounds similar to an offset, but there are some important differences.

Key considerations with redraw:

- Access can be restricted or delayed depending on the lender

- Some lenders limit how much you can redraw or how often

- Funds are technically the bank’s, not sitting in your own account

- Can create complications if used incorrectly (especially for investment purposes)

Offset vs Redraw: What’s the Real Difference?

When comparing offset vs redraw, it comes down to control, flexibility and strategy.

| Feature | Offset Account | Redraw Facility |

|---|---|---|

| Access to funds | Immediate | May be restricted |

| Ownership of funds | Yours | Paid into the loan |

| Flexibility | High | Medium |

| Tax clarity (for investors) | Clean | Can get messy |

| Fees | Sometimes higher | Usually lower |

At a basic level, both reduce interest, but strategically, they’re not interchangeable.

When an Offset Account Makes More Sense

An offset account is usually the better option if:

- You want full control over your cash

- You’re planning to turn your home into an investment later

- You want maximum flexibility with your money

- You’re building a long-term property portfolio

This is where structure matters and why you need to speak with an expert lending adviser. It’s no use getting the lowest interest rate if it restricts you from being able to leverage your own money and equity you have in property.

We often see people accidentally limit their future options simply because they didn’t think about how their loan setup would affect them later.

When Redraw Might Be Enough

This doesn’t mean an offset account is perfect for everyone all the time because of the flexibility. Sometimes, a redraw facility can work well too.

When a redraw facility might be better:

- You’re focused purely on paying down your loan faster

- You don’t need frequent access to the extra funds

- You want to avoid higher loan fees

- Your situation is simple and unlikely to change

For some borrowers, that’s perfectly fine. For others however, it can become restrictive at the worst possible time.

The Hidden Trap Most People Miss

Then there’s the time where offset vs redraw really matters.

Do you ever plan to:

- Invest in property?

- Upgrade your home?

- Access equity later?

If so, your loan structure today can either help or hurt you.

For example, using redraw incorrectly can create tax complications down the track, whereas an offset account keeps things clean and flexible. This is one of those areas where a small decision now can have a six-figure impact over time.

Offset vs Redraw: Which One Is Better?

Unfortunately, there’s no one-size-fits-all answer.

But here’s the simplest way to think about it:

| Offset | Redraw |

|---|---|

| Flexibility + Strategy | Simplicity + Cost Efficiency |

| ✅ Full access to your cash | ✅ Directly reduces your loan balance |

| ✅ Useful for property investors & upgraders | ✅ Keeps your loan fees lower |

The right choice depends on what you’re trying to achieve and not just what saves you a few dollars today.

Final Thoughts

When it comes to offset vs redraw, most people focus on interest savings, however the real advantage comes from choosing the structure that supports your future plans. This is where good advice makes a difference.

Ideally, you want to set yourself up to be in a better position for the future and not just to try and save a few dollars on interest month to month.

Need Help Structuring Your Loan Properly?

If you’re not sure whether an offset account or redraw is right for you, it’s worth getting clarity before you lock anything in. A quick conversation now can save you a lot of time, money and stress later. Speak to Indigo Finance and get your loan structure right from the start.