New rules for investment lending from 1 February: what investors should know

Over the last few year we’ve seen an increase in activity amongst Australian property investors – including heavier gearing.

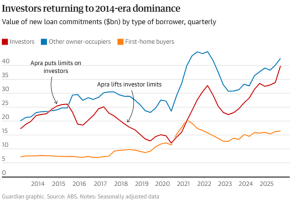

In the September 2025 quarter, investors made up around two in every five new home loans, even as first homebuyer activity softened and property values continued to rise across much of the country.

From 1 February 2026, new APRA investment lending rules — including a debt-to-income (DTI) cap — will change how banks assess and approve lending for property investors. These changes come at a time when affordability pressures remain high and investor activity continues to outpace income growth.

The result is a shifting lending environment that investors need to understand clearly before planning their next move.

What’s changing from 1 February 2026?

APRA (the Australian Prudential Regulation Authority) is introducing limits on how much high debt-to-income lending banks can write.

At the same time, government policies continue to support highly leveraged entry into the market for first home buyers through low-deposit and shared equity schemes.

For growth-focused investors, this combination means credit access may become more constrained and more policy-driven — even where repayment histories and buffers are strong.

What is APRA’s debt-to-income (DTI) cap?

A debt-to-income (DTI) ratio compares a borrower’s total debt to their gross annual income.

From 1 February 2026, APRA will require authorised deposit-taking institutions (ADIs) — including major banks and most mainstream lenders — to limit high-DTI lending so that no more than 20% of new mortgage loans are written at a DTI of six times income or higher.

This limit:

- is applied separately to owner-occupiers and investors

- applies only to ADIs (not non-bank lenders)

- is designed to reduce the build-up of higher-risk lending

APRA has been clear that the aim is to support long-term financial stability by containing riskier lending — particularly as investor borrowing has grown faster than incomes.

In practice, as banks approach their high-DTI limits, they may become more selective about which applications they approve, prioritising lower-risk or more profitable borrowers.

Why do these investment lending rules matter for property investors?

Property investors often operate at higher DTIs than owner-occupiers because each additional property adds debt faster than income typically grows.

This is especially true in markets such as Sydney, Brisbane and Melbourne, where property values have increased more quickly than wages.

As a result, portfolio investors — particularly those with four or more properties — are more likely to encounter tighter lending conditions under the new rules, even if they have strong repayment histories and substantial buffers.

The concern isn’t that high-DTI investment loans will disappear altogether. Rather, access may become:

- less consistent between lenders

- more sensitive to timing within a quarter

- increasingly influenced by internal bank policy

Investment lending rules vs first home buyer schemes

While APRA is tightening settings around high-DTI lending, government policy continues to support higher leverage for first home buyers through initiatives such as:

- The 5% deposit guarantee, allowing eligible buyers to avoid lenders mortgage insurance

- Shared equity programs, such as Help to Buy, where the government contributes up to 30–40% of the purchase price

These schemes reduce deposit barriers and bring buyers into the market earlier, but they also embed households in highly geared positions relative to income and savings.

This contrast — restraint for investors alongside leverage for new buyers — has renewed debate about affordability, risk and longer-term outcomes.

Ongoing debate around risk and affordability

Some industry commentators have highlighted the tension between APRA’s focus on systemic stability and policies that encourage low-equity entry into the market.

There are concerns that buyers entering with deposits of 2–5% may be more exposed to negative equity if property values soften or employment conditions change — particularly compared to established investors who have accumulated equity over time.

Others question whether these schemes improve affordability in a lasting way, or whether they simply pull demand forward and add pressure to entry-level housing stock, particularly in markets where price caps sit close to median values.

Banks are tightening on trusts and company borrowers

Alongside the new DTI cap, many lenders are also taking a more conservative approach to trust and company borrowing structures.

This can include:

- stricter income assessment methods

- higher interest rate buffers

- reduced recognition of potential tax benefits, such as negative gearing

Rather than assuming full and consistent tax refunds, lenders may apply haircuts to these benefits — or exclude them entirely — when assessing serviceability.

Combined with the DTI cap, this means some investors who have historically relied on complex structures may see reduced borrowing capacity with mainstream lenders over the next lending cycle.

What property investors can do now

As investment lending rules evolve, the focus is shifting from simply maximising borrowing capacity to structuring lending strategically.

For investors looking to continue building portfolios, priorities may include:

- staying informed about APRA and lender policy changes

- understanding how different lenders assess DTI and structures

- maintaining flexibility as non-bank and specialist options evolve

Non-bank lenders are not directly subject to APRA’s DTI cap, but they price for risk. Higher rates and fees need to be weighed carefully against long-term portfolio goals, with conservative buffers built in.

Frequently asked questions about the new investment lending rules

Are high-DTI investment loans being banned?

No. High-DTI lending will still be available, but banks will be limited in how many of these loans they can approve.

Do these rules apply to non-bank lenders?

No. Non-bank lenders are not bound by APRA’s DTI cap, though they often charge higher rates and fees to reflect risk.

Will this affect existing loans?

No. The DTI cap applies to new lending only. Existing loans are not impacted.

Staying flexible in a changing lending environment

As banks tighten policies and lending conditions become more selective, flexibility is increasingly valuable.

Investors who plan ahead, understand lender differences and build buffers into their strategy are better positioned to adapt — even as investment lending rules in Australia continue to evolve.

The information in this article is general in nature and provided for informational purposes only. It does not take into account your individual objectives, financial situation or needs.

Before making any lending or investment decisions, it’s important to seek advice tailored to your circumstances. An Indigo Finance Lending Adviser can help you understand how these changes may apply to you.