Cost of Living Pressure Is Forcing Lenders to Adapt

If you’ve been feeling the cost of living pressure recently, you’re not alone and it’s something that is very real. The big question is, how has it been affecting budgets, borrowing and loan approvals? Here’s what it means for you and how lenders are responding.

What Is the Cost of Living Pressure?

Every monthly bill adds up. From groceries and fuel to rent and energy, households across Australia are feeling squeezed. Some price jumps are obvious, like your weekly grocery bill. Others creep up slowly and you hardly notice. That is until you wake up one day and feel like you are drowning.

Pressures add up over time. Your costs are rising, but your income likely isn’t keeping pace. The standard of living you have become used to now begins to become further out of reach. Here are some of the phases most households go through:

- You can no longer save as much as you once did

- Then you are no longer able to save at all

- You start eating into any investments you may have previously had

- Debt starts to increase

- Cut backs are made on luxuries such as holidays and eating out

- Budget cuts are made on things like insurances and monthly expenses

- You find yourself at a point where the numbers no longer add up

And it doesn’t matter if you are comfortably on six-figures, or living paycheck to paycheck. The story remains the same.

Invariably, cost of living pressure means households must juggle more expenses, making home loan repayments tougher than ever.

However, when you factor in interest rates and borrowing capacity, that’s not the entire picture either.

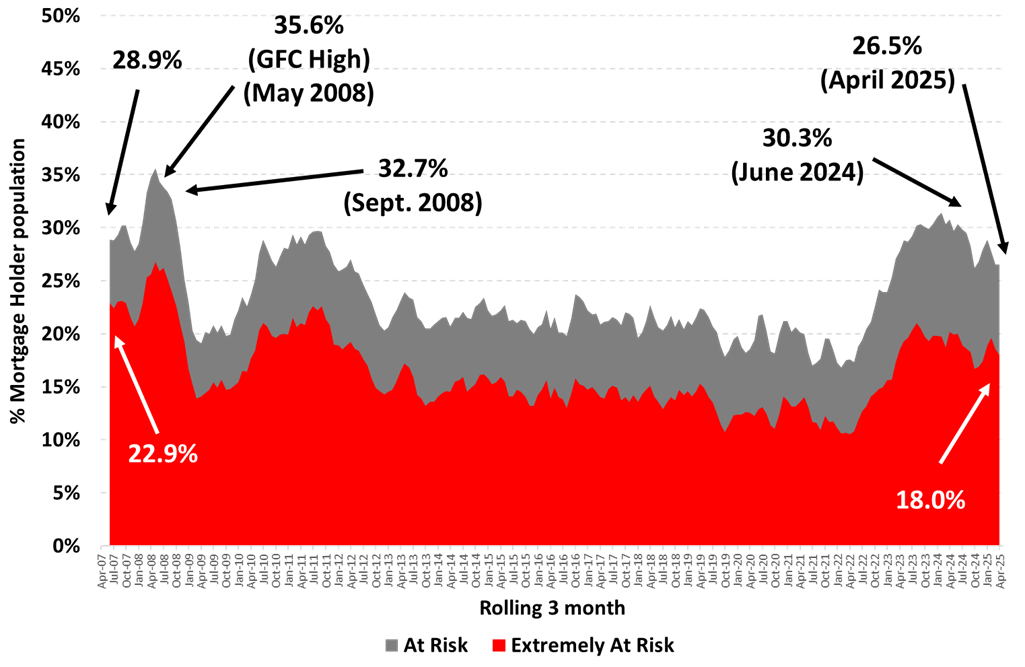

Mortgage Stress

While the cost of living pressure rises, so does mortgage stress. Prior to interest rate cuts earlier this year, 30.3% of owner occupied mortgage holders were considered “at risk” of mortgage stress. So if you’re feeling the pinch, you’re not alone.

Fortunately, the rate cuts have also taken the pressure off mortgage stress with that figure now dropping to 26.5%. While this doesn’t represent a complete easing of circumstances, it’s certainly a step in the right direction.

Source: Roy Morgan

Meanwhile, renting hasn’t eased either, with median rent now sitting around $620 per week. Property prices continue hovering around $1m in major cities.

How Are Lenders Responding to Cost of Living Pressure?

With the rising cost of groceries, fuel, rent and utilities hitting household budgets hard, lenders are having to walk a fine line. On one hand, they’re tasked with maintaining responsible lending practices. On the other, they can’t ignore the financial strain borrowers are under.

In response to this pressure, banks and regulators are making subtle but significant changes behind the scenes. These changes are reshaping who can borrow, how much they can access, and what hoops they need to jump through to get a loan approved.

Here are some of the pieces of the jigsaw:

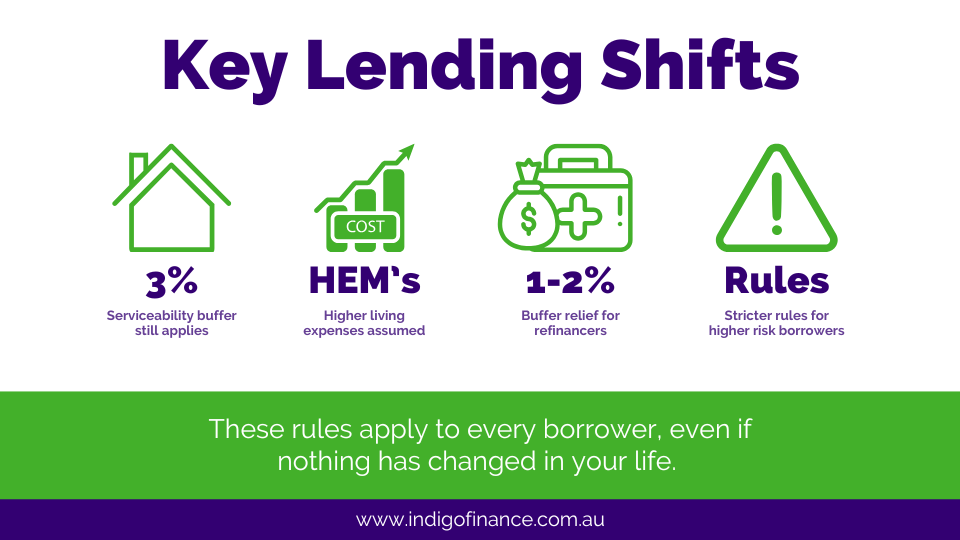

Maintaining serviceability buffers

Despite calls from some corners of the industry (and members of the government) to ease serviceability rules, APRA has continued to enforce a 3% buffer on top of a borrower’s actual interest rate when assessing a new loan. This is designed to protect borrowers from future rate rises or unexpected expenses, ensuring they don’t take on more debt than they can handle.

Raising Household Expenditure Models (HEMs)

To reflect the real cost of living, many lenders have updated their internal household expense benchmarks. In practical terms, this means they’re assuming you’ll need more to live on each month. This in turn reduces your borrowing capacity accordingly, however as interest rates fall, many borrowers may actually find their borrowing capacity increasing. Confused? This is why everyone should be talking with a lending adviser about their specific circumstances.

Offering buffer relief for refinancers

In a rare show of flexibility, some lenders have started offering relief for refinancers. This has been applied mainly to those looking for a like-for-like loan. Instead of applying the full 3% buffer, they may assess serviceability with a 2% or even 1% buffer in certain cases. Keep in mind it’s not automatic, and it doesn’t apply to everyone. However, we’ve seen it as a helpful tool for clients ranging from struggling borrowers to those refinancing strategically.

Tightening credit for higher-risk borrowers

While some relief is being offered, banks are also becoming more selective. Those with high debt-to-income ratios, unstable employment, or multiple credit lines are facing more scrutiny. In some cases, this means outright declines. In others, it means tougher documentation requirements or reduced borrowing limits. Risk appetite across lenders has dropped and some borrowers are feeling it.

These changes can be confusing if you’re not in the industry day-to-day. Lenders are taking the cost of living crisis seriously. They’re balancing financial stability with borrower needs. This means personalised lending advice is more important than ever.

Impact on Borrowers and What You Need to Know

The consequence of cost of living pressure and tighter lending rules is real. If you’re planning to buy, invest, or refinance, here’s what it could mean for you:

- Your borrowing capacity may drop, especially if you’re already stretched. Lenders now assume you’ll be spending more just to live day to day, which leaves less room to repay a loan.

- Repayments will feel heavier with higher assumed living expenses built into calculations. Even if nothing has changed in your real-world budget, the bank’s model sees it differently.

- However… tighter cost of living pressure might mean banks are more shy to lend, however as interest rates lower, we’re still seeing increased borrowing capacity for clients when their loans are structured effectively.

A real world hypothetical example

Let’s take a look at an example of a fictional Sydney couple between 2022 and 2025. We’ll assume they have a combined gross income of $160k.

In mid 2022, interest rates were lower, so assessments were often based on actual rates + a 2.5% buffer. Today, APRA has made the 3% buffer as a minimum. So a 2.5% home loan rate was assessed at 5%, while a 6% rate today is assessed at 9%.

With the increase in HEM values, lenders now assume much higher monthly spending. A $3,500 monthly spend for this couple in 2022 might now be assessed at closer to $4,500 or $5,000 a month, depending on the lender and postcode. This increase directly reduces the income available to service the debt.

| 2022 | 2025 | |

|---|---|---|

| Combined Net Monthly Income | $12,306 | $12,306 |

| Assumed Monthly Living Costs | $3,500 | $5,000 |

| Remaining for Loan Repayment | $8,806 | $7,306 |

| Assessment Interest Rate | 5.0% | 9.0% |

| Max Loan (30 yrs P&I) | ~$700,000 | ~$635,000 |

(This is a fictional example based on rounded off figures using broad assumptions)

Again though, this is a comparison with when interest rates were lower. Given that we’ve seen interest rates fall from a high recently, when today’s figures are compared to those before the interest rate cuts, borrowing capacity is now higher, despite the increase in assumed spending.

To make matters even more challenging for a couple right now, if one of the partners is casual or has contract based work (or if they have existing liabilities like credit cards or car loans), the bank will factor those in as well.

If the loan assessment is pushed below $600,000 (in the example above), the couple could fail serviceability altogether.

Even if they don’t have much debt, the higher assessment rate and HEM eats away at their borrowing capacity.

What Borrowers Can Do to Offset the Pressure

Feeling the squeeze doesn’t mean you’re out of options, especially with interest rate cuts. In fact, understanding the levers you can pull might make all the difference. There are a number of different strategies you can use to offset the lending challenges you might currently face.

Refinance to a Better Loan

With interest rates falling again and some lenders sharpening their offers to attract business, refinancing remains a smart move. In fact, the RBA’s rate cut in April 2025 sparked a 6.5% increase in refinancing activity, according to CoreLogic.

For many, switching lenders can reduce repayments, access better features, or even unlock cashback offers. Just be sure to compare the full cost, not just the rate.

Track Living Costs

If lenders are tightening their scrutiny of your expenses, so should you.

Start by reviewing your last 3 to 6 months of spending. Identify subscriptions, entertainment, or takeout habits that can be trimmed. Even small changes can improve your affordability and help you build a repayment buffer, which lenders view favourably.

When you’re preparing to get pre-approval, it’s often wise to decrease credit card limits too. Even if you have a perfect credit record, lenders see loan limits as access to finance and can assume you have maxed these out when assessing your borrowing capacity.

Explore Different Loan Terms

If you’re struggling to meet repayments, some lenders offer 35 or even 40 year loan terms. These reduce monthly payments by stretching them out over a longer period.

It’s not ideal for those wanting to pay down debt fast, but in today’s climate, it can be a helpful short-term strategy for cash flow relief.

Your borrowing strategy should align with your personal financial goals. Far too many people simply take a loan without considering the long term ramifications on their family’s wealth. Smart people plan for the future.

Look for Policy Exceptions

Some lenders still provide flexibility under APRA’s exception framework. This can particularly apply for strong applicants who fall just short of policy.

This might include:

- Accepting different types of income (e.g. contract, self-employed)

- Allowing larger debts if offset by strong savings

- Reducing buffer rates for low-risk refinancers

The key is working with a lending adviser who knows how and when to request exceptions. This is often where strategy beats rate.

Do You Speak to a Mortgage Broker or Lending Adviser?

In this climate, professional advice matters more than ever.

A mortgage broker can show you product comparisons.

However a lending adviser does more than compare rates. They help you understand buffer risks, cost implications, and long-term goals.

If you’re getting the picture that you definitely need help understanding your options, then you’re on the right path. There’s simply no way the average person could get their head around all the nuances of lending. Understanding how to navigate all the tricks can make a massive difference to your cash flow and financial future.

The lending squeeze is on, but with those being offset by interest rate cuts, smart clients are using it to their advantage.

Lenders are tightening, buffers stay high and borrowing capacity is shifting. With the right guidance, you can find a strategy that works for you.

Now is the time to talk with a lending adviser if:

- Cost of living is putting on the squeeze

- You haven’t looked into refinancing in over 12 months

- Circumstances have changed

- You want to re-visit your long term strategies and goals

- You are looking to become (or refinance as) a Business Owner and Home Owner

Let’s work through a smart plan together. It costs nothing to have a chat and see how we can help.