How Often Should You Do a Mortgage Review in Australia?

Most Australians set up their home loan then don’t even consider a mortgage review for years.

That can be expensive.

Interest rates move, property values change and lenders release new loan products all the time. So borrowers who never check their mortgage often end up paying a “loyalty tax” simply for staying where they are and don’t even realise it.

They’re literally handing free money to the banks that they are entitled to keep in their own pockets.

What’s mind-blowing is when people drive out of their way to save 4c per litre on petrol, though don’t even consider spending that same amount of time to save thousands per year on their mortgage.

A quick mortgage review with a broker or lending adviser and you could be putting that money straight back in your pocket, often without changing lenders.

So how often should you review your mortgage, and what difference can it actually make?

Why a Mortgage Review Matters

Many borrowers assume their bank will automatically keep their loan competitive. Think about how ridiculous that sounds. Surely you’ve seen countless media articles talking about record bank profits, right? Where do you think those profits come from?

In reality, lenders rarely are looking out for mortgage holders interests as a priority. They have shareholders to look after.

Lenders often offer their best rates to new customers, while long term borrowers slowly drift onto higher rates over time.

The Australian Government’s financial guidance service, MoneySmart, says there can be more than a 2 percent difference between home loan rates on the market, which can translate into significant long term costs.

Even a small rate gap can have a large impact.

On a $700,000 mortgage, reducing your interest rate by just 0.5 percent can save around $3,000 per year in repayments. Larger reductions can save far more.

That is why regular mortgage reviews are one of the simplest ways to keep your loan competitive.

How Often Should You Review Your Mortgage?

For most borrowers, a mortgage review every 12 months is a sensible rule. Many smart investors check in bi-annually.

This allows enough time for market changes, rate movements, or property value changes to create opportunities for savings.

You should also consider a loan review if:

- Your fixed rate period has ended

- Interest rates have moved significantly

- Your property has increased in value

- Your loan balance is still large

- Your income or financial position has improved

Even if you ultimately stay with your current lender, reviewing your mortgage ensures your rate remains competitive.

How Often Australians Actually Review Their Loans

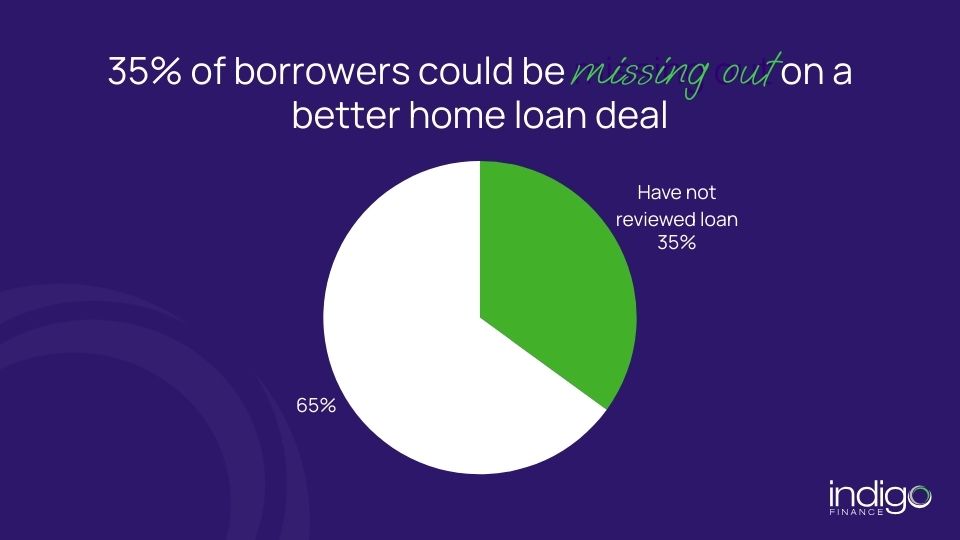

Despite the potential savings, many Australians rarely check their home loan.

Research from Mortgage Choice found around 35 percent of borrowers had not reviewed their mortgage in the past 12 months, meaning a significant portion may be paying more than necessary.

At the same time, refinancing activity has surged.

The Australian Banking Association reported over 640,000 mortgages were refinanced in 2025, reflecting a growing awareness among borrowers that better deals may exist.

Yet millions of borrowers still remain on loans that may no longer be competitive.

How Much Could a Mortgage Review Save?

The savings from a mortgage review depend on several factors, including the size of your loan and the difference between your current rate and available rates.

For context, the average new home loan in Australia is about $693,000, according to lending data.

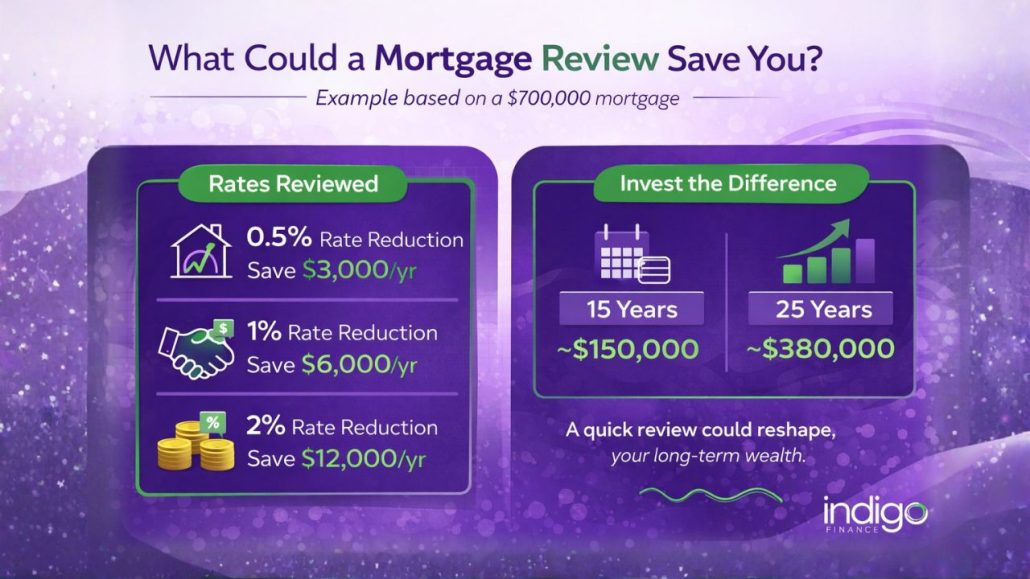

Let’s look at the potential impact of different rate reductions on a $700,000 loan:

0.50 percent rate reduction = about $3,000

1.00 percent rate reduction = about $6,000

2.00 percent rate reduction = about $12,000

These savings can be substantial.

But the real impact becomes clear when you consider what that money could become over time.

What If You Invested the Savings Instead?

Imagine a borrower saved $6,000 per year after a mortgage review and invested that amount each year instead. If that money earned an average return of 7 percent annually, after 15 years it could grow to roughly $150,000.

After 25 years, that could become more than $380,000 through compound growth.

In other words, a simple mortgage review today could quietly reshape a household’s long term wealth.

How a Mortgage Review Looks Behind the Scenes

Let’s say you had a loan of just over $1 million with a major lender.

We’ll assume you’ve been with that lender for several years and simply took it for granted that their rate was already competitive.

How would you check?

The good news is, there’s not a great deal you need to do.

One phone call to your lending adviser, providing a recent loan statement and confirming your current loan details is all it takes to get the ball rolling.

Then, behind the scenes, your lending adviser will check:

- Your current interest rate

- Available rates from their lender

- Competing lenders in the market

- Your loan to value ratio and equity position

Rather than refinancing straight away, the lending advisers first step would be to approach your existing lender. Often negotiating with them is the simplest way to reduce your repayments.

Many lenders will generally agree to reduce your interest rate (in some cases by around 2 percent) just to retain the loan.

- No refinancing required

- No valuation needed

- No application process

- Just a rate adjustment

If your current lender doesn’t come back with the best deal, your lending adviser will put together suggestions and alternatives mapping out options to change lender and what that means for your back pocket.

Often there’s times where refinancing can produce even more significant savings.

This entire process can take anywhere from a few hours to a week depending on the value of, and how complex the loans are.

And the outcome often results in reduced mortgage payments (many times thousands of dollars per year) and your money remaining in your pocket, rather than being paid to the lender.

All it takes to get started is one phone call.

Signs It Is Time to Review Your Mortgage Now

If any of the following apply, it may be worth reviewing your loan sooner rather than later:

- You have not reviewed your mortgage in the past 12 months

- Your interest rate seems higher than current market rates

- Your loan is over $500,000 or $1 million

- Your property value has increased significantly

- Your fixed rate has recently expired

A quick mortgage review can reveal whether there is an opportunity to reduce your repayments or improve your loan structure.

Most Australians would be shocked what a single phone call to your lending adviser could yield in saved repayments.

Just Remember

Your mortgage is often the largest financial commitment you will ever have, yet many borrowers spend more time comparing phone plans or electricity providers than they do reviewing their home loan.

A simple annual mortgage review can help ensure your rate remains competitive and that your loan structure still suits your financial goals.

Sometimes the outcome is small, or you discover you are already on the best rate with the best package.

Other times, a phone call can save thousands. Either way, it is one of the easiest financial check ups you can make.

So rather than just reading this article and being entertained, call Indigo Finance right now on 02 9194 2260, or contact Indigo Finance and we’ll show you how simple this process can be. You have absolutely nothing to lose, but could be the hero of your household budget if you’re currently missing out.