The Real Cost of Buying a Home in Australia

Most people think the biggest cost of buying a home is saving the deposit, but that’s only part of the story.

When purchasing a property in Australia there are a range of additional costs that many buyers do not anticipate. These include government charges, legal fees, inspections, bank costs and other expenses that appear during the settlement process.

Understanding these costs early can help you plan properly and avoid surprises.

Let’s take a look at the breakdown of the most common costs associated with buying a home in Australia today.

1. Deposit

The deposit is the largest upfront cost when purchasing a property.

Most lenders prefer a deposit of 20 percent of the purchase price, although it is possible to buy with a smaller deposit (especially if you work with a good lending adviser).

Example

Property price = $1,000,000

20 percent deposit = $200,000

If your deposit is less than 20 percent, you may need to pay Lenders Mortgage Insurance (LMI). There are also advantages first home buyers unlock if they take part in the government first home owner scheme.

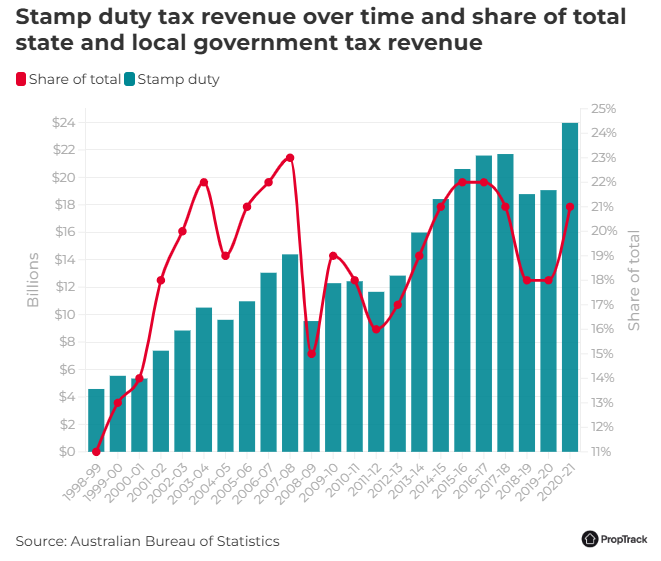

2. Stamp Duty

Stamp duty is a state government tax applied when property changes ownership. Yes, it’s literally a government tax on the stamp that is applied to the paperwork. And if you think it’s a lot, you’d be right. In NSW alone, stamp duty accounts for roughly 22% to 30%+ of the annual government budget (depending on how many properties change hands).

This is usually the second largest cost after the deposit, however the actual amount depends on:

- the state or territory

- the purchase price

- whether you qualify for first home buyer concessions

Example in NSW

Property price = $1,000,000

Estimated stamp duty = About $40,000

Because stamp duty can be a significant cost of buying a home, it is important to include it in your budget early in the buying process. Once again though, there are some state based schemes to reduce stamp duty for first home owners, making the cost of buying a home a little less daunting. For example, here is a link to find out more about the First Home Buyers Assistance scheme.

3. Conveyancing or Legal Fees

When purchasing property you will need a solicitor or conveyancer to manage the legal side of the transaction.

This includes:

- reviewing the contract of sale

- conducting legal searches

- preparing settlement documents

- coordinating with the bank and selling agent

Typical cost = $1,500 to $3,000

4. Building and Pest Inspections

Before committing to a property purchase it is important to understand the condition of the building. A building inspection identifies structural issues while a pest inspection checks for termite activity or damage.

Spending a few dollars here can save thousands (and up to millions – yes millions) in headaches once the keys are handed over.

Typical cost

Building inspection = $400 to $800

Pest inspection = $250 to $500

Many providers offer a combined building and pest inspection.

5. Lenders Mortgage Insurance (LMI)

If you borrow more than 80 percent of the property’s value, the lender may require Lenders Mortgage Insurance.

This insurance protects the lender, not the borrower, in the event the loan cannot be repaid.

Example

Property price = $1,000,000

Deposit = $100,000

Loan = $900,000

Estimated LMI = $20,000 to $30,000

In many cases this cost of buying a home can be added to the loan rather than paid upfront.

It’s a unique part of what separates “getting a loan” and “working with an expert lending adviser”. If you simply go to get a loan and don’t understand how LMI works, you will almost surely end up in a worse position than if you work alongside someone who understands how LMI works like the back of their hand.

6. Government Registration Fees

When property changes ownership, the government charges registration fees to update official records.

Common fees include:

Mortgage registration fee = About $170 to $200 in NSW

Transfer registration fee = About $170 to $200 in NSW

These fees vary slightly by state.

7. Bank Fees

Depending on the lender and loan product there may be additional loan related costs.

Examples include:

- loan application fees

- settlement administration fees

- valuation fees

Many lenders might waive these costs, but they can still add several hundred dollars.

Typical range = $0 to $600

8. Property Searches and Certificates

Your conveyancer will order several official searches to ensure there are no legal issues with the property.

These may include:

- title search

- council certificates

- zoning checks

- water authority certificates

Typical cost = $200 to $500

These are often included within conveyancing fees, though it’s important to understand the breakdown.

9. Strata Inspection Report (Units Only)

If you are buying an apartment or townhouse within a strata scheme, it is important to review the strata records.

A strata inspection report can reveal:

- upcoming special levies

- building defects

- disputes within the building

- the financial health of the strata fund

Typical cost = $200 to $400

Once again, a huge “insurance policy” so you can avoid any unwanted (and expensive) surprises.

10. Settlement Adjustments

At settlement, the buyer reimburses the seller for certain prepaid expenses.

These may include:

- council rates

- water rates

- strata levies

Depending on the timing of settlement this may add hundreds or even thousands of dollars to the final settlement figure. If you are tight on your budget and haven’t allowed for the smaller details, you could be left in an extremely awkward position.

11. Moving Cost of Buying a Home

Moving costs are often overlooked when budgeting for a property purchase.

Examples include:

- removalists

- truck hire

- packing materials

- storage

Typical cost = $500 to $3,000 depending on the size of the move.

Again, this is something we see people overlook all the time. They don’t consider the time, or expenses associated with their move. Even if you plan on doing it yourself, you still need a means of transport and all the packing materials. Moving expenses can add up very fast.

12. Home Insurance

Most lenders require home insurance to be in place before settlement.

Typical cost = $800 to $2,000 per year depending on the property.

Yes, this is an ongoing expense, but you will likely need to show proof of insurance before settlement. It’s yet another cost that has to come from your pocket.

13. Immediate Post Purchase Costs

After moving in, many buyers face additional expenses.

Examples include:

- changing locks

- small repairs

- new appliances

- furniture

- internet setup

These costs vary widely but can easily run into several thousand dollars. For many people, it’s ok to push back basic upgrades and fixes, however there’s always going to be expenses you haven’t foreseen.

Example Total Cost of Buying a Home

For a $1,000,000 property purchase in NSW, the upfront costs could look something like this.

Deposit

$200,000

Stamp duty

$40,000

Conveyancing

$2,000

Building and pest inspections

$600

Government fees

$350

Insurance

$1,200

Moving costs

$1,500

Other costs

$1,000

Estimated total upfront funds required

Around $245,000

Where Do You Start?

Buying property involves far more than just saving the deposit. If you’re smart from day 1, you’ll be able to navigate the process without any nasty surprises. Government charges, legal fees, inspections and settlement adjustments can add tens of thousands of dollars to the total cost of purchasing a home. Understanding these expenses ahead of time can help buyers plan properly and avoid unexpected financial pressure during the buying process.

If you are unsure how these costs apply to your situation, speaking with an experienced lending adviser can help you understand the full financial picture before you commit to a purchase.