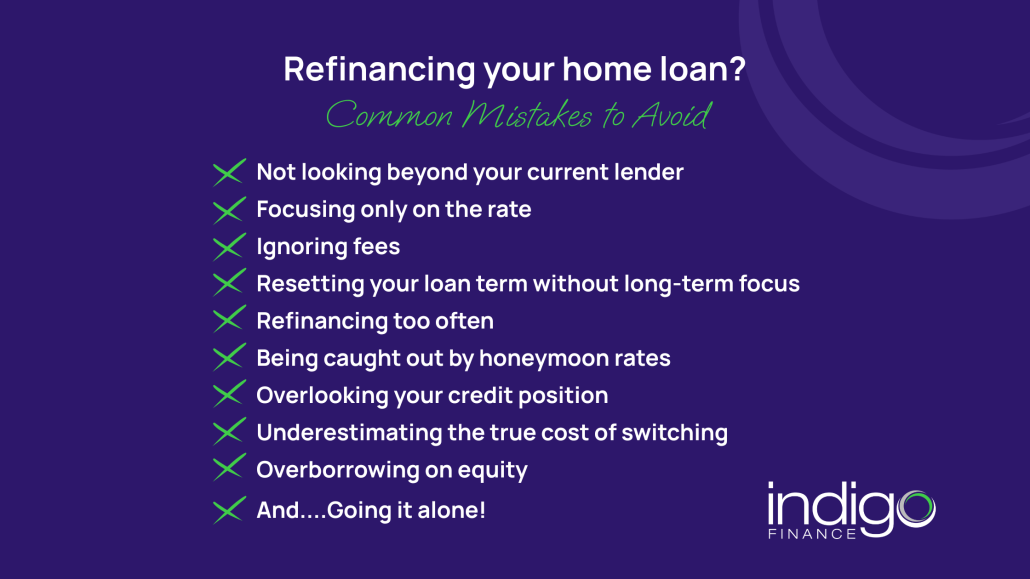

Refinancing your home loan: common mistakes to avoid

Refinancing is often talked about as an easy way to save money, unlock equity or improve your loan features.

And sometimes, it is.

But in practice, we regularly see Australians refinance with good intentions — only to end up paying more than expected, or missing out on better options because key details were overlooked.

If you’re thinking about refinancing, these are some of the most common mistakes we see, and why they matter.

Mistake 1: Not looking beyond your current lender

It’s surprisingly common for people to refinance without really shopping around.

Rates, fees and lending policies can vary widely between lenders. Even a small difference can add up over time. Staying with your existing bank out of convenience or loyalty doesn’t always deliver the best result — especially in a market that’s constantly changing.

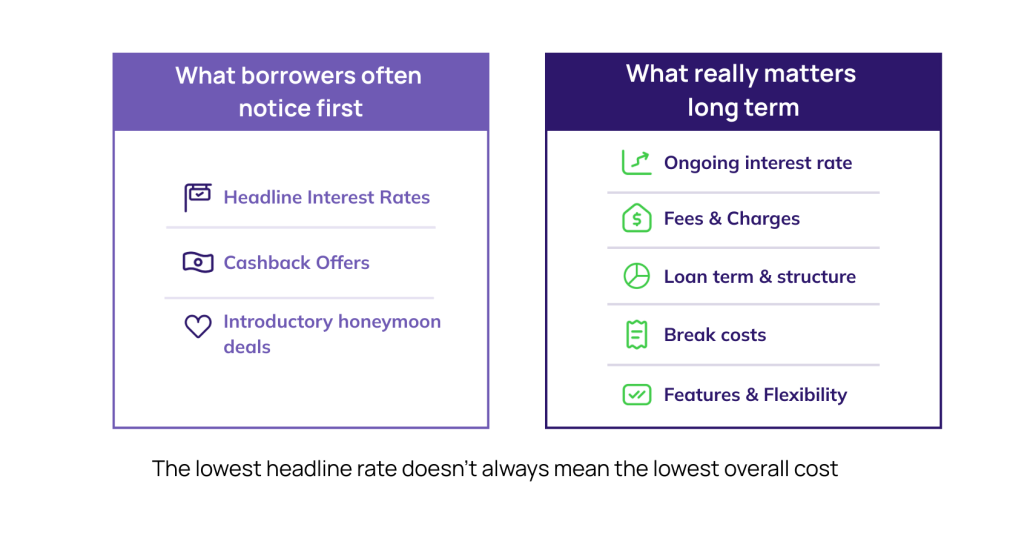

Mistake 2: Fixating on the headline rate or cashback

A low interest rate or a generous cashback can grab attention quickly. But those numbers rarely tell the full story.

Fees, ongoing costs and loan features all play a role in what a loan actually costs over the long term. Comparison rates can be a useful sense check, and it’s worth considering whether short-term incentives truly outweigh longer-term value.

Mistake 3: Resetting the loan term without thinking it through

Lower repayments can feel like a win. But restarting your loan term — for example, turning 25 years remaining back into a new 30-year loan — can quietly increase the total interest you’ll pay over time.

Refinancing works best when the loan structure reflects where you want to be in the future, not just what feels easiest right now.

Mistake 4: Refinancing too often

When rates are moving, it can be tempting to keep switching lenders in search of a better deal.

The catch is that each refinance can come with costs, such as application fees or mortgage discharge fees. If you’re not careful, those costs can cancel out the savings you’re chasing.

Mistake 5: Being caught out by honeymoon rates

Introductory or “honeymoon” rates can look very appealing at first glance. The problem is what happens after they end.

Many revert to higher ongoing rates, which can leave you worse off if you’re not paying attention. Always check what the loan looks like once the introductory period is over.

Mistake 6: Overlooking your credit position

Some borrowers only discover credit issues once their application is already underway.

Checking your credit file early can help avoid surprises, delays or declined applications. It’s also wise to space out loan applications, as multiple enquiries in a short period can affect approval outcomes.

Mistake 7: Underestimating the true cost of switching

Refinancing isn’t free — and the costs can start to mount up. Depending on your current loan, you may need to factor in:

-

settlement fees

-

break costs (especially on fixed-rate loans)

-

valuation fees

-

lender discharge fees

Take the time to weigh these costs against the potential savings to help ensure refinancing your home loan actually makes sense.

Mistake 8: Borrowing more equity than you need

Accessing equity can be useful, but borrowing too much starts to introduce risk; property values could fall or your income could change.

Keeping future repayments manageable and maintaining flexibility will make a big difference over time.

Mistake 9: Going it alone

Refinancing is about more than just chasing after a lower rate. The features of your new loan, policies and long-term flexibility all matter.

Having experienced guidance can help you avoid common mistakes and make more informed decisions.

A more confident approach to refinancing

Refinancing can be a powerful tool when it’s done thoughtfully. By avoiding these common mistakes and taking a considered approach, you’re far more likely to end up with a loan that genuinely supports your financial goals — now and into the future.

Want to find out more? Reach out to one of our Lending Advisers and we can help you find the best path forward with your home loan.