First Home Buyer Scheme 2025: What You Need to Know

Buying your first home is one of the biggest financial steps you’ll ever take. It’s a complex process that most people don’t fully understand until they have to go through it. Did you know that if you’re a first home buyer, there’s a first home buyer scheme, along with other benefits you can take advantage of?

On October 1st 2025, the federal government is making big changes to their Home Guarantee Scheme. It’s a scheme that has been around for some time, though due to restrictions, it has been becoming more and more difficult for first home buyers to take advantage of it. Income caps for singles and couples have meant that many miss. Then even for the lucky ones that did qualify under the income cap, the property price cap has meant that in markets like Sydney, buying under the scheme was still quite difficult.

So this week, we sat down with Priya Deguara, who is one of our incredible lending advisers here at Indigo Finance and asked her to explain the changes and to tell us more about how she’s been helping our first home buyer clients maximise their buying potential.

Here’s what we learned from the conversation and why these new changes are such a game changer for some first home buyers.

At Indigo Finance, we see clients come to us all the time oblivious to the savings they could make, plus how much easier it could actually be to save a deposit. Not to mention how overwhelming the whole first home buyer scheme process is.

Understanding the Changes to the First Home Buyer Scheme

Understanding the First Home Buyer Scheme updates in 2025 can mean the difference of tens of thousands of dollars for first home buyers. With changes rolling in from 1 October 2025, there are real opportunities to make home ownership more accessible. Higher property price caps under the federal Home Guarantee Scheme, the removal of income limits, unlimited scheme places, and updates to how HECS-HELP debts are treated all combine to bring more buyers into the market. At the same time, the state-based NSW First Home Buyers Assistance Scheme continues to offer stamp duty exemptions and concessions, but under different thresholds.

At Indigo Finance, our role is to help you navigate these changes so you can plan properly, avoid unexpected risks, and get the maximum benefit. In this article, I’ll cover:

- Why pre-approval matters more than ever

- How the First Home Buyer Scheme is changing in 2025

- How Lender’s Mortgage Insurance (LMI) works and how to avoid it

- What stamp duty exemptions really mean in practice

- What other benefits are available for a first home buyer

- The role of lending advisers in maximising benefits

- Practical tips from our experience with first home buyers

Why Pre-Approval is Critical for First Home Buyers

At Indigo Finance, Priya and the team are always adamant with first home buyers that they get pre-approval before putting down a deposit. Without it, you can end up in urgent situations, with limited options, or even risk losing money.

Priya noted that sometimes we see clients put down deposits without pre-approval, which creates pressure. Many assume their income alone determines what they can borrow. The reality is lenders also factor in liabilities like HECS-HELP, unused credit card limits, and car loans. That means the amount you think you can borrow often ends up being less once everything is included.

The real danger comes when buyers find their dream property and make an offer without pre-approval. They think finance will be simple, only to discover later that their borrowing power falls short. At that point, the clock is ticking, and they’re left scrambling to secure finance before it’s too late.

Why pre-approval matters:

- Clarity on borrowing power

- you’ll know what you can spend before you make offers.

- Protection against urgent situations

- no last-minute scrambling once a contract is signed.

- Stronger negotiating position

- sellers and agents take you seriously when you’re pre-approved.

- Time to improve your position

- we can help you reduce credit card limits, choose lenders who treat HECS more favourably, or tidy up other liabilities.

Recent changes make this even more important:

- Some banks have announced they will exclude HECS-HELP repayments from loan assessments if the balance is under $20,000, verified with ATO records.

- Other lenders will exclude HELP debt if it can be repaid within 12 months (Finspo).

- From 1 October 2025, the federal Home Guarantee Scheme will expand with higher price caps and no income caps (Housing Australia).

Pre-approval isn’t just a formality. It’s the foundation for buying with confidence.

Priya Deguara is a first home buyer expert lending adviser for Indigo Finance

Understanding the Federal First Home Buyer Scheme Changes in 2025 (Home Guarantee Scheme)

The federal government scheme has to do with Lender’s Mortgage Insurance, otherwise known as LMI.

Many people think you need a 20% deposit in order to qualify for a loan to buy property, but it’s just not true. Even for first home buyers. With as little as 5% deposit, some banks will lend you the other 95% if you show you can service the loan, as long as you pay LMI.

Lender’s Mortgage Insurance (LMI) Explained

LMI is one of the most misunderstood costs. It protects the lender, not you, and is charged when your deposit is less than 20 percent. On an $800,000 property with a 10 percent deposit, it can be more than $20,000.

It’s an upfront payment you make and you never see that money again.

The federal Home Guarantee Scheme allows you to avoid this cost by buying with as little as a 5 percent deposit and no LMI. That saving alone can be the difference between waiting years or getting into the market sooner.

How the First Home Buyer Scheme Helps

From 1 October 2025, Priya explains that the scheme will allow unlimited first home buyers to access the guarantee with no income caps and higher property price caps. That means more buyers can use it to avoid LMI while putting down just 5 percent. (Housing Australia)

To put it in real terms:

- If you’re buying a $900,000 home and you’ve saved $45,000 (a 5% deposit), the scheme allows you to go ahead without LMI.

- Without the scheme, you’d usually need $180,000 saved for a 20% deposit or be forced to pay LMI on top of your smaller deposit.

That’s why so many of our first home buyer clients see the scheme as their best way into the market.

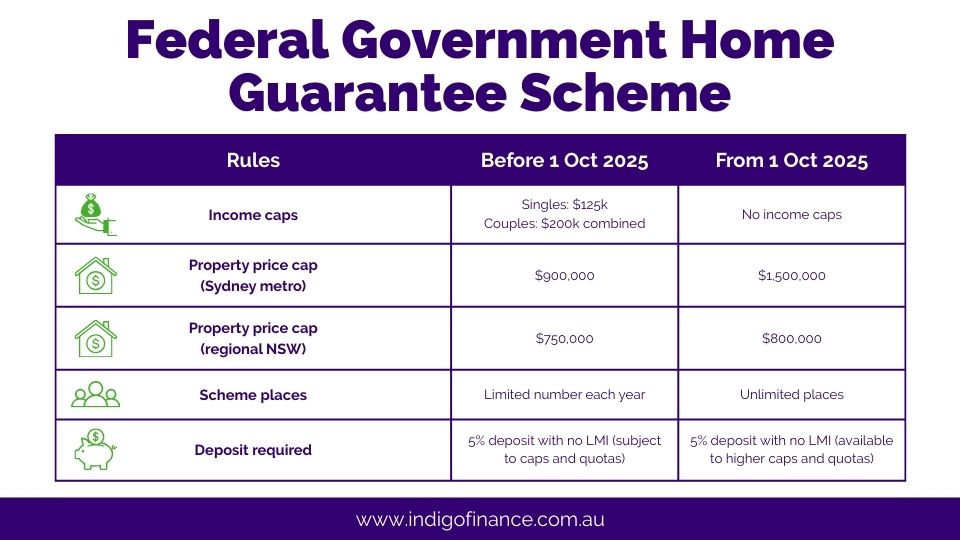

From 1 October 2025, the First Home Buyer Scheme (part of the federal Home Guarantee Scheme) is being overhauled. Here are the changes being made:

- Unlimited places

- No more missing out because the quota is full.

- No income caps

- Higher-income earners can now qualify.

- Higher property price caps

- In NSW, the cap rises from $900,000 to $1.5 million for Sydney metro areas.

- 5% deposit without LMI

- Buyers can enter the market sooner without paying Lender’s Mortgage Insurance.

- Simplified regional rules

- The scheme is being streamlined so regional buyers face fewer complications.

Before vs After (Federal Scheme – Home Guarantee Scheme)

These changes are significant because if you tap into the benefits, you can ultimately stretch your property buying budget. But remember that lenders still apply their own criteria when approving loans. Credit history, liabilities, and documentation all still matter, so when it comes time to get your finances in order, preparation is key.

What Hasn’t Changed (Important to Know)

While many things are improving, some rules remain the same, and others may depend on your situation or lender:

- You still need to satisfy lender requirements around credit history, liabilities (like HECS/HELP), income verification, etc. Even though some policy changes help reduce the burden, lenders still assess prudential risk.

- Residency and “moving in” conditions for state-based assistance (like transfer duty / stamp duty exemptions) often still require that you move in within a set time and live there continuously.

- Eligibility rules around who qualifies as a “first home buyer” (e.g. not having previously owned property, being a citizen or permanent resident, etc.) remain in place for most of the schemes.

Stamp Duty Exemptions for First Home Buyers in NSW (State Scheme)

Priya suggests there are two important things to note:

- This state scheme is completely separate to the federal government Home Guarantee Scheme

- This scheme is not changing on 1 October 2025

However, as it works hand in hand with the federal LMI scheme and can be stacked together for even more considerable savings, it’s important to cover again.

Stamp duty is one of the biggest upfront costs that buyers face. As the name suggests, it’s literally a very expensive tax you pay for a “stamp” on your contract. Thankfully, the First Home Buyers Assistance Scheme (FHBAS) in NSW offers major relief.

Although these details are not changing, it’s important to know about them.

- Buy a new or existing home valued up to $800,000 and you pay no stamp duty.

- Buy between $800,001 and $1,000,000 and you’ll pay a reduced (concessional) rate.

- For vacant land, it’s exempt up to $350,000 and concessional up to $450,000 (Revenue NSW).

How Do You Qualify?

Qualification varies from state to state, however generally speaking, there are a few key things to remember. To be a part of the scheme, applicants must:

- Be over 18 and a permanent resident or citizen.

- Never have owned property in Australia.

- Move in within 12 months and live there for at least 12 months.

For many first home buyers, this stamp duty concession can be a saving of $30,000 to $40,000 (sometimes more). We help clients check the numbers carefully, since even a small drop in purchase price can push you under the exemption threshold.

What It Means in Practice

To clarify the figures above and because of the current thresholds, in NSW:

- If you buy a home (new or existing) valued at $800,000 or less, you pay no stamp duty under FHBAS.

- If the home is between $800,001 and $1,000,000, you still get a concession (a reduced duty), not full exemption.

- For vacant land you plan to build on if it’s:

- valued up to $350,000, you get full exemption

- between $350,001 and $450,000, you pay the concessional rate

- above $450,000, there is no concession.

- Even when the property value is high, but you cross the thresholds just a little, it can make a big difference. So it is worth checking exactly where the value of the property you’re considering sits.

Other First Home Buyer Benefits You Can Use

Alongside the federal Home Guarantee Scheme and NSW stamp duty exemptions, Priya clarifies that there are other supports worth knowing about too. These can often be combined to reduce your upfront costs even further.

First Home Owner Grant

If you’re buying or building a new home, you may be eligible for a state based first home buyers grant. In NSW, for example, the property must be valued at $600,000 or less for a new home, or $750,000 or less for a house-and-land package. This payment goes straight toward your costs at settlement.

First Home Super Saver Scheme (Federal)

The First Home Super Saver Scheme lets you save your deposit through superannuation. You can contribute up to $15,000 per year (and $50,000 total), then withdraw it later to buy your first home. Because super contributions are taxed at 15% instead of your usual income tax rate, this can be a smart way to save faster.

Shared Equity Options (NSW)

The NSW Government has run shared equity programs for single parents, older singles, and key workers. These aren’t open to everyone, but if you qualify, the government contributes up to 40% of the property price in exchange for an equity share. That means you borrow less, and your repayments are smaller.

Other Lender Incentives

Some banks also waive fees or reduce interest rates for first home buyers. While not as large as government benefits, they’re worth factoring into the total picture.

The NSW government tool “Home Buyer Assistance Finder” can help you check whether you’re eligible for FHBAS, the Grant, and other state-level assistance.

The Role of Lending Advisers in Maximising First Home Buyer Benefits

You might think buying a home is just about going to a bank and getting a loan approved, but decisions you make now can have huge ramifications on how you borrow and build wealth in the future.

The biggest mistake young people make is that they just walk into their local bank without understanding there are literally hundreds of different loans in the market that could be better suited to their needs.

This is where a good lending adviser is worth their weight in gold.

Access to More Lenders, More Options

Our lending advisers at Indigo Finance, including Priya, work with more than 60 lenders, which means that instead of being restricted to one bank’s policies, we can compare across the market. This matters to first home buyers because:

- Different banks treat liabilities like HECS and credit cards differently.

- Some lenders will allow higher borrowing capacity than others based on your profile.

- Interest rates and fee structures vary widely between lenders.

By comparing across multiple banks, we can often find options that save you money, increase your borrowing power, or both. It might not seem like it makes a difference now, but the right loan structures can make a huge difference in years to come.

Securing Scheme Places

One thing many buyers don’t realise is that the First Home Buyer Scheme is accessed through your lender, not directly from the government.

Speak to your lending adviser and they can secure your scheme place as part of your application. That’s a crucial step, because missing out on the scheme could cost you tens of thousands in LMI, stamp duty, or mean you need a bigger deposit than you planned.

FAQ’s About the New First Home Buyer Scheme

When we asked Priya what the most common questions were, as well as the questions people might not know to ask, but should, she was quick to highlight the following:

Q: What date actually matters: contract exchange, settlement, or application?

A: The application date is what counts (however it must occur before the settlement date). If your lender submits your scheme application before 1 October 2025, you’ll be assessed under the current rules, however if it’s submitted on or after 1 October, you’ll be under the new rules. Contract and settlement dates don’t decide which scheme you’re in.

Q: What if I exchanged contracts before 1 October but haven’t settled yet?

A: If your application was lodged before 1 October, it will sit under the current rules. But because you haven’t settled yet, your lender may be able to re-work your application once the new rules begin. This has to be done before your settlement date.

Q: What if I already have a scheme place under the old rules?

A: You can keep it as is, or you may ask your lender to reapply after 1 October so it falls under the new rules. Again, this option is only available if you haven’t yet settled.

Q: Can I apply for the new scheme before 1 October?

A: No. Lenders cannot submit applications under the new scheme until 1 October. Anything lodged before then is locked into the current rules unless it is re-applied for later (and before settlement).

Q: Can I switch to the new scheme after I’ve already settled?

A: No. Once settlement has happened, you can’t change or reapply. The scheme must be in place before settlement.

Q: Should I hold off buying until after 1 October?

A: You don’t have to. Given the current date (as of time of publication) being so close to the date of the new scheme, your settlement date is going to occur after 1 October anyway. Speak with your lending adviser on how to coordinate your application.

Q: Do all lenders participate in the scheme?

A: No. Not all lenders. This is why you need an expert lending adviser to help guide you through the process.

Practical Tips for First Home Buyers

At Indigo Finance, we always tell first home buyers that success is about preparation. The more you know up front, the fewer surprises you’ll face once you’re in the middle of contracts, inspections, and loan approvals. Based on our experience working with hundreds of first home buyers, here are the key things we’d encourage you to focus on:

- Speak to your Lending Adviser first

- Get clarity on your borrowing power before looking at properties.

- Don’t assume income alone means borrowing power

- Liabilities like HECS and credit limits matter.

- Understand the residency rules

- You must live in the property to keep your benefits.

- Be smart about your deposit

- Budget for extra costs, not just the deposit.

- Think long-term

- Choose a property that works now and into the future.

The federal scheme changes coming in October make this one of the best times for first home buyers in years. Unlimited scheme places, higher caps, no income limits, and the chance to avoid LMI are major benefits. And when combined with the state’s stamp duty exemptions (where your property is $1m or less), the savings can be significant.

Details Matter

Residency conditions, lender rules, liabilities, and timing all need to be handled properly. That’s where an experienced lending adviser comes in.

Sure, you can try to navigate this yourself, but we’ve seen way too many people come to us who’ve either made a mistake, or missed all the benefits they should have claimed.

At Indigo Finance, we’re here to help you every step of the way. Team members like Priya, with her understanding of the market are crucial in your property journey. They can show you options you may never consider or have access to, plus walk you through all the potential government benefits and schemes that can seem so complex (or that you didn’t even know about).

We can explain how this all works and what it means to you in plain English, from pre-approval, through scheme applications and onto settlement.

Put yourself in the strongest position possible and make the journey smoother and less stressful.

It’s free to reach out and see what this means for you. We’re happy to help. If you’d like to speak with Priya directly, give us a call on +61 9194 2260.