If you’re thinking about buying property, you’ve probably heard the term “pre-approval” mentioned before. But what exactly is pre-approval and what does it mean for you?

Simply put, a home loan pre-approval is when a lender agrees in principle to lend you a certain amount of money before you’ve found your ideal property. It helps you understand your borrowing capacity and can make the home buying journey much smoother.

If you know how much you have to spend, you know what you can offer.

What is Pre-Approval and Why Does It Matter?

Pre-approval is about having the confidence to make an offer on a property, knowing what the bank is willing to lend you. It tells sellers and agents that you’re serious and ready to buy.

However, a pre-approval isn’t an agreement to loan you the money. It’s just an indication from a lender that they would be willing to loan you the money for a suitable property if your income and circumstances don’t change.

Effectively, a pre-approval means the bank is highly likely to loan you the money… but it’s essential to remember that it’s never a guarantee and especially not if your income or circumstances change before you go for full approval.

Having said that, knowing how much you can borrow helps you shop within your budget, reducing stress (and potential disappointment) down the track.

Key Benefits of Getting Pre-Approval

Know Exactly What You Can Afford

We constantly meet people who are searching for property and have absolutely no idea what the bank would be willing to lend them. Sometimes, clients have come to us saying they’ve already found their dream home, only to face the reality that they can’t get a mortgage to buy it.

It’s an uncomfortable scenario, though one that can be easily avoided if you simply go through the pre-approval stage first.

Boost Your Negotiating Power

Imagine you are a selling agent and have two people wanting to make an offer on a property. One has pre-approval. The other does not. Which potential buyer are you going to spend time with? Sellers love pre-approved buyers because it shows they are serious and gives a degree of certainty.

When you’re pre-approved, you can also confidently negotiate on price and terms. Having that confidence can often give you a buying advantage in the market too. You’d probably be surprised how many people say they are “looking” for property, though in reality aren’t even close to making an offer.

Speed Up Your Buying Process

If you’ve already gone through the pre-approval stage, your finance application is already halfway there. This means that if you find the property you wish to buy, you can move quickly, reducing the risk of missing out in a fast-moving market.

When Should You Get Pre-Approval?

The Right Timing for First Home Buyers

If you’re entering the property market for the first time, you should seek pre-approval early, before you even start your search. This gives you clarity and sets realistic expectations about your buying power, helping you target suitable properties (and in which locations). Understanding the amount you are looking to borrow helps give you a realistic idea of what properties you are actually going to be able to buy.

Many first home buyers fall into the trap of starting their search before pre-approval, only to discover later that they have been looking at properties they are unable to afford. That might be because they are looking at properties which are too expensive, or in an area their budget won’t stretch to.

Getting Pre-Approved Before Selling Your Current Home

Selling your current home and buying a new one can be a stressful time. Juggling how your loans fit into this equation is something best left to the experts. You need to understand that if you sell one property and buy another, it has massive ramifications on your mortgage. It’s not as easy as keeping the same loan and not even having to let the bank know.

For this step, you’re going to need to understand your options and that’s best done with an expert lending adviser.

If you already own a property, pre-approval helps you understand how much you can spend on your next home (even if your current home hasn’t sold yet). This reduces the stress of juggling buying and selling simultaneously, even if the loans themselves might become a bit of a jigsaw puzzle.

Pre-Approval for Investors

If you’re considering investing in property, obtaining pre-approval is a smart and strategic first step. It gives you a clear understanding of your borrowing power, enabling you to quickly capitalise on investment opportunities as they arise.

It doesn’t matter whether you’re using home equity to invest in property, or are rentvesting and building your portfolio, the principles remain the same.

Pre-approval positions buyers favourably in negotiations, showing sellers and agents that they are serious. Money talks.

Most importantly though, any good investor will tell you that planning your portfolio is possibly the most important skill you need to understand. Knowing your borrowing power allows you to not only plan your portfolio better, it also ensures you can target the right properties that align with your financial goals.

Here are the top tips we were recently given by a property buyer’s agent for those looking to invest in property:

- Get your finances in order so you know exactly how much you can spend

- Know exactly what type of property you are looking to buy and where

- Research sold listings so you know what you want is available and what price you will need to pay

- Be ready to take decisive action when the right property arises

The best deals in property always go to those who are on the spot and ready to act when they arise. By the time most “mum and dad” investors are ready to make an offer, a decisive investor has already done the deal and taken that property off the market.

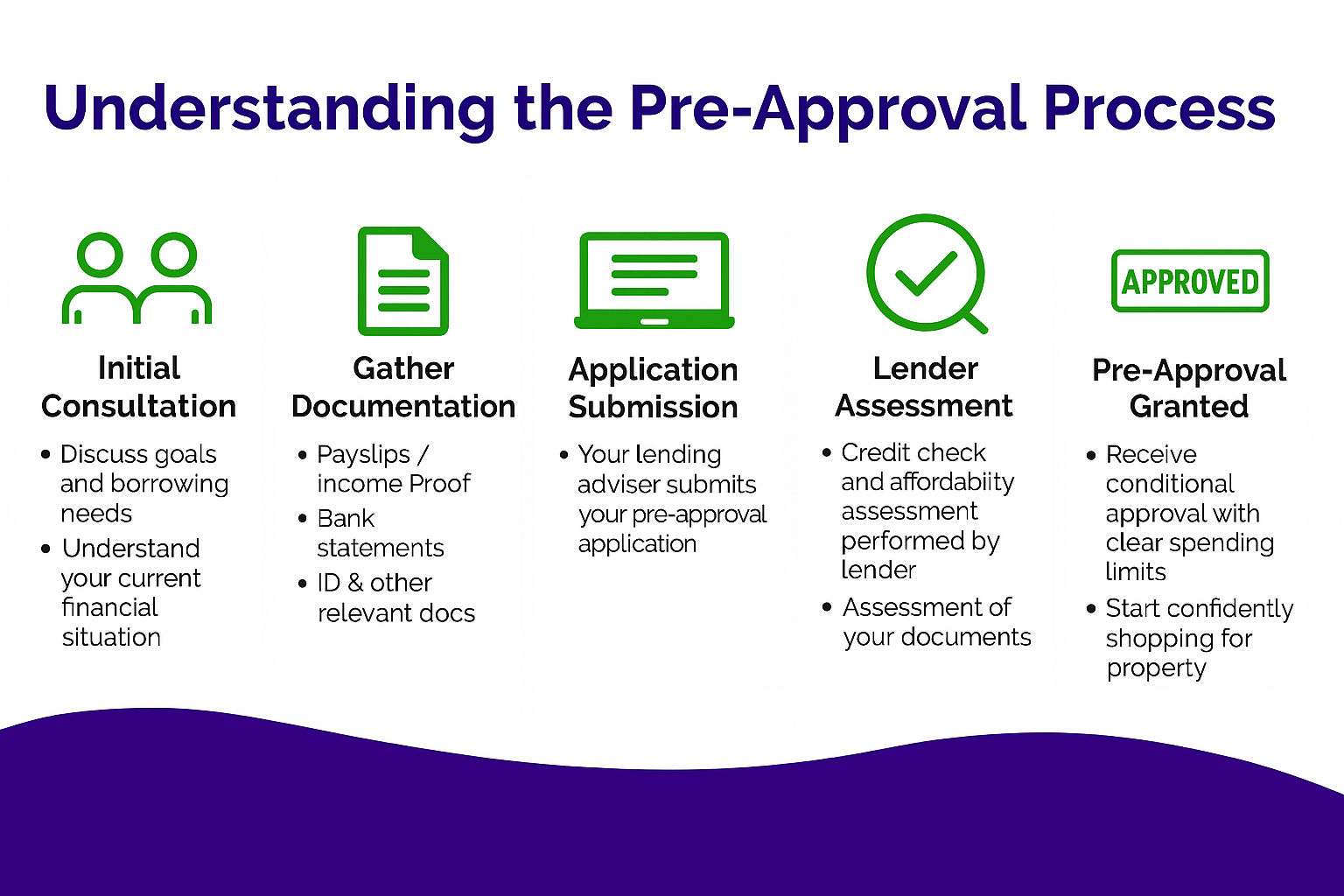

Understanding the Pre-Approval Process

What Documents Do You Need for Pre-Approval?

For anyone who has been through the pre-approval phase before, you’ll know that you need to have your documentation in order. Good mortgage brokers and lending advisers make this much easier with advanced systems and automations.

If you’re putting together your own documents, you’ll typically need:

- Proof of income (payslips or tax returns)

- Bank statements

- Details of existing debts

- Identification documents

How Long Does the Pre-Approval Process Take?

Once your mortgage broker or lending adviser has your documents, pre-approval generally takes about 1 to 7 business days. However this can vary depending on the lender, your financial situation and the complexity of your application. Let your lending adviser walk you through this early.

Does Pre-Approval Guarantee a Home Loan?

As we said before, a pre-approval is NOT a guarantee. Final approval depends on factors like the property’s valuation, your employment (or earnings) and personal circumstances remaining stable.

It should also be noted that just because a lender has said they would lend you, say $1m, if you bid $1m on a home at an auction that is valued by the bank at $800k, then you could find yourself in a very tricky spot. It’s essential you don’t overpay on a property. Banks will only lend you up to what they think is a fair price.

How Does Lenders Mortgage Insurance (LMI) Affect Pre-Approval?

If your deposit is less than 20% of the property’s value, your pre-approval may be subject to Lenders Mortgage Insurance (LMI). LMI is a one-off insurance premium that protects your lender (not you) if you’re unable to repay your loan.

LMI can significantly impact your borrowing capacity, although can also be leveraged as a tool if you know how to use it correctly. Either way, it’s something that will be factored into your pre-approval.

Here’s a few things to consider if applying for pre-approval with potential for LMI:

- Factor in the additional cost of LMI, as it can increase your total borrowing amount

- You need to understand all the costs of buying property, not just the actual purchase value

- Understand that the insurer’s approval is separate from your lender’s approval and that could impact your final loan decision

- Be aware that there are certain property types or valuations that can affect your eligibility for LMI

What most people don’t understand is that there is a “sweet spot” when it comes to LMI and using it effectively can make huge differences to borrowing capacity and long term portfolio projections. Also, knowing how LMI works with your pre-approval helps avoid unexpected hurdles when securing your home loan.

Conditions that Might Impact Your Approval

It’s important to be aware of conditions that could change your loan capacity in the short term. Speak to your lending adviser about the following:

- Changes in employment

- New debts (including increased credit card limits)

- Property valuations coming in below expectations

- Changes in relationship or family status

Any of these can affect your final approval and you need to know where you stand.

Common Mistakes People Make with Pre-Approval

Assuming Pre-Approval Lasts Forever

Pre-approvals definitely don’t last forever. It’s extremely common to find people who have their pre-approval lapse. Sometimes it’s because life got in the way, they don’t find the property they were after, or they are looking for a property that simply doesn’t exist.

An expired pre-approval is not the end of the world, but if it happens, you need to start the entire process again.

You definitely don’t want to get caught out and find the property of your dreams only to realise your pre-approval has lapsed and therefore miss out to another buyer who does have their finances in order.

Keep in mind, pre-approval typically lasts 3-6 months depending on the lender. Don’t assume your pre-approval will be valid indefinitely. Always confirm its validity period and be sure to mark the dates in your calendar.

Misunderstanding the Difference Between Pre-Approval and Final Approval

Remember how we mentioned that pre-approval is conditional and not guaranteed? Final approval only happens after your offer on a property is accepted and your lender completes all necessary checks. You can’t actually get final approval until the bank is able to look specifically at the property they are lending on.

That’s why it’s essential to make sure you don’t overpay for a property.

Trusting a System-Generated Pre-Approval

Not all pre-approvals involve a real person reviewing your application. Some are fully automated and can miss key details — like whether your income has been accurately assessed, if the property meets lender policy, or whether rental yields are realistic (especially for investors).

A pre-approval that hasn’t been human-reviewed can lead to nasty surprises at the final approval stage. Always ask: Has a person actually looked at this?

Not Realising That Property Types Can Affect Approval

Did you know that small studio apartments or rural properties might impact your ability to secure a loan? Even if you’ve been pre-approved? Just remember that details can vary between properties and states. So it’s essential to speak with your mortgage broker or lending adviser to help you understand your specific circumstances.

Mortgage Broker vs Lending Adviser: Who Should Handle Your Pre-Approval?

While a traditional mortgage broker will present loan options, a lending adviser provides strategic advice tailored to your unique financial situation. When it comes to finance, you are going to be far better off if you understand the bigger picture with a lending adviser, rather than just shooting for the lowest interest rate.

If you’ve ever asked yourself “do I need a mortgage broker or lending adviser”, your first step is likely to learn exactly what each of them does. Educate yourself. Most people make the biggest purchases of their lives and spend less time on it than they do on securing petrol at a 4c per litre discount.

What Happens After You Get Pre-Approved?

Setting Your Realistic Property Budget

Just because you get pre-approved for say, $1m, it doesn’t mean you should spend $1m. Use your pre-approval limit to set a realistic budget.

Plus, you need to remember to factor in additional costs like:

- Stamp duty

- Conveyancing and legal fees

- Building and pest inspections

- Strata inspections (if applicable)

- Valuations

- Buyer’s agent fees (if applicable)

Many buyers fall into the trap of spending the absolute maximum, just because it’s available and often, this is not a great financial choice. Only by speaking with qualified experts will you get the right advice for your circumstances.

Remember, no matter how convincing they might sound, your next door neighbour is not an expert.

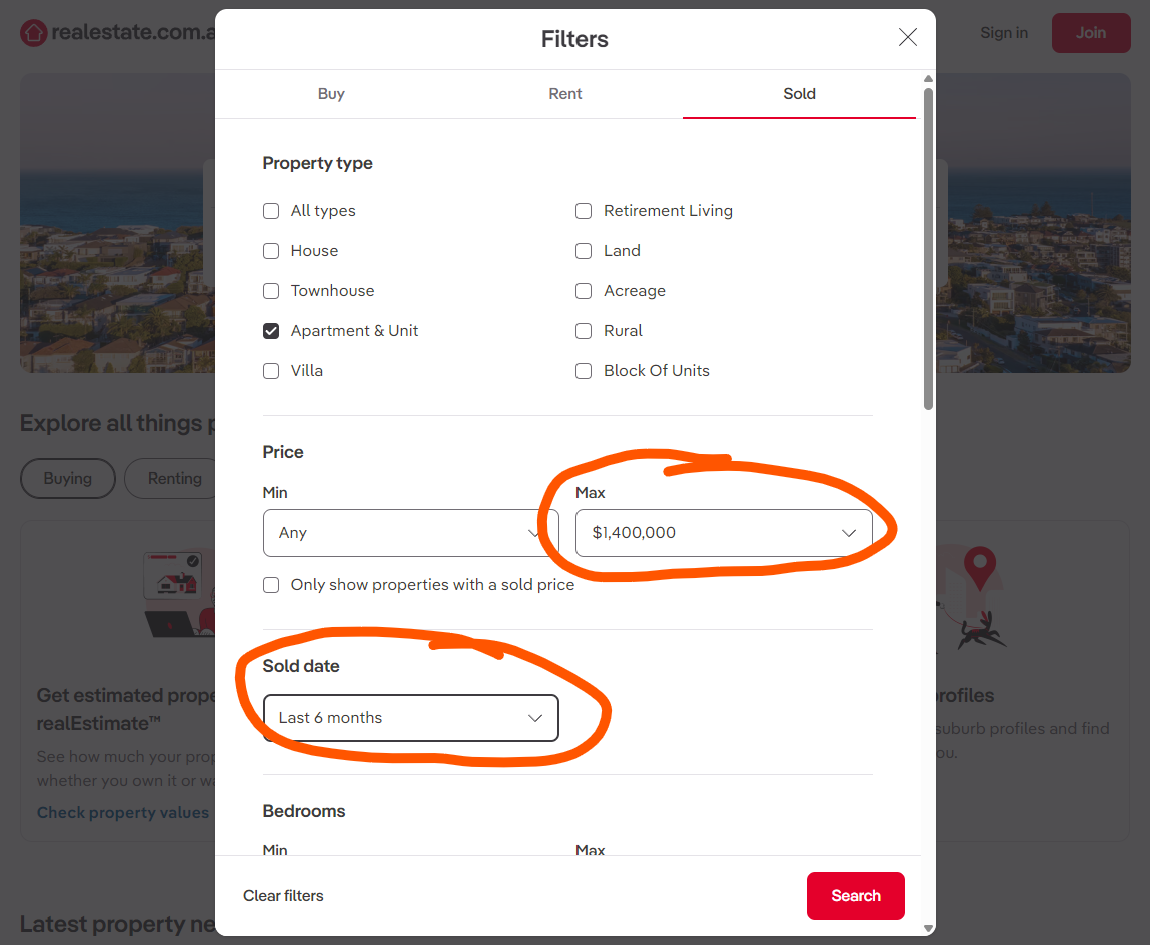

Finding the Right Property

Once you’ve got a clear budget, head to Domain or RealEstate and do the following search:

- Sold properties

- Properties for sale are NOT an accurate representation of what they are worth. You only get that from looking at what something actually sold for

- Price

- Select the Max price that is within your budget (not above)

- Sold date

- Select “Last 6 months”, because the price of anything sold longer than that ago could be vastly different today

With a clear budget and an understanding of what properties are actually being sold for, your property search becomes more targeted and efficient, saving valuable time and effort.

Making an Offer with Confidence

When you do find the right property, you’ll be ready to confidently make an offer, backed by your pre-approved finance.

Once you know how much money you actually have to spend, your offers will become more decisive. In the real estate world, this is good for both you and the sellers, often resulting in a better deal for both parties.

How? Because you can often get the property for a better price or on better terms because the seller has confidence that the offer is genuine.

Why Pre-Approval Could Be Your Best Move

Think of pre-approval as strategic planning. It’s not just putting a number on a piece of paper. It prepares you financially and mentally, giving you a significant edge in today’s competitive property market.

At Indigo Finance, we specialise in providing comprehensive lending advice and pre-approval services tailored specifically to you. Don’t just ask for the lowest rate. Instead sit down with a specialist and map out your financial goals.

If you want to get an idea of what you could potentially borrow for a new home or investment property contact Indigo Finance. Get your own personalised pre-approval consultation today.