https://www.indigofinance.com.au/wp-content/uploads/2018/02/IF-Topic-Sheet.png

328

255

IndigoFinance

https://www.indigofinance.com.au/wp-content/uploads/2017/01/indigo-finance-logo.png

IndigoFinance2018-03-19 20:14:422018-03-19 20:14:51The power in your equity

https://www.indigofinance.com.au/wp-content/uploads/2018/02/IF-Topic-Sheet.png

328

255

IndigoFinance

https://www.indigofinance.com.au/wp-content/uploads/2017/01/indigo-finance-logo.png

IndigoFinance2018-03-19 20:14:422018-03-19 20:14:51The power in your equity https://www.indigofinance.com.au/wp-content/uploads/2018/03/IF-case-study-1.png

315

560

IndigoFinance

https://www.indigofinance.com.au/wp-content/uploads/2017/01/indigo-finance-logo.png

IndigoFinance2018-03-11 15:37:312018-03-11 19:00:36Could you turn one property into six within a decade? Meet one couple who did

https://www.indigofinance.com.au/wp-content/uploads/2018/03/IF-case-study-1.png

315

560

IndigoFinance

https://www.indigofinance.com.au/wp-content/uploads/2017/01/indigo-finance-logo.png

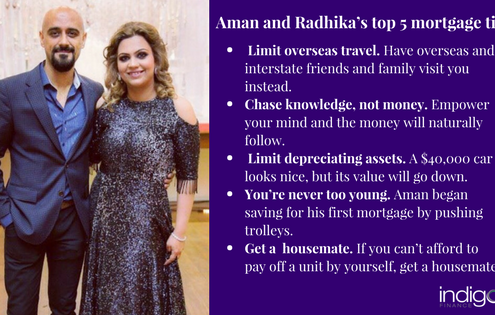

IndigoFinance2018-03-11 15:37:312018-03-11 19:00:36Could you turn one property into six within a decade? Meet one couple who did https://www.indigofinance.com.au/wp-content/uploads/2018/03/IF-05-02-18.jpg

357

728

IndigoFinance

https://www.indigofinance.com.au/wp-content/uploads/2017/01/indigo-finance-logo.png

IndigoFinance2018-03-04 19:04:422018-03-04 19:04:42Think you need to be wealthy to invest?

https://www.indigofinance.com.au/wp-content/uploads/2018/03/IF-05-02-18.jpg

357

728

IndigoFinance

https://www.indigofinance.com.au/wp-content/uploads/2017/01/indigo-finance-logo.png

IndigoFinance2018-03-04 19:04:422018-03-04 19:04:42Think you need to be wealthy to invest?